The Foothill Premium: Pricing Sensitivity and Geohazards in Almaden Valley

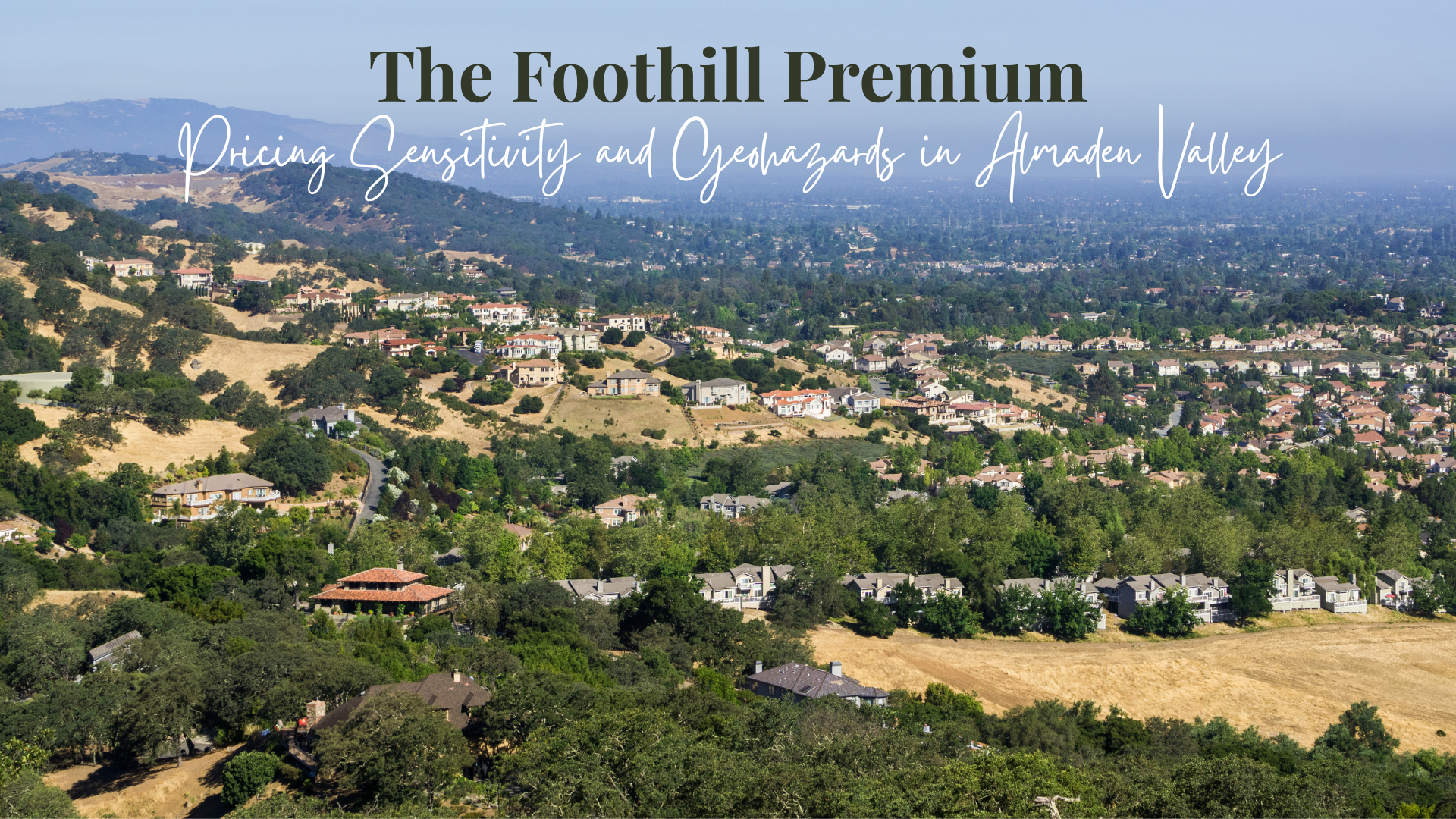

Tucked into the scenic southwestern foothills of San Jose, Almaden Valley has long commanded a distinct "foothill premium" . Homebuyers are drawn to this prestigious enclave for its larger lot sizes, custom single-family estates, top-performing schools, and immediate access to beautiful open spaces.

However, in mid-2026, the Almaden Valley market is undergoing a serious reality check . High-income buyers and sellers are navigating a changing local landscape shaped by a massive realignment of Silicon Valley tech wealth and a complex home insurance market.

Whether you are looking to sell a multi-million-dollar estate or purchase your dream home in the foothills, here is a simplified, jargon-free breakdown of what is actually happening on the ground.

Part 1: The Neighborhood Pricing Gradient

Almaden Valley’s natural topography is one of its greatest financial drivers . As you move away from the flat valley floors of South San Jose and ascend into the rolling hills, home values shift dramatically:

- The Foothill Elevation Premium: Entering the foothills of Almaden Valley (95120) typically drives home values 35% to 50% higher than standard homes on the flat valley floor.

- The Geospatial Hierarchy: To put this premium into perspective, Almaden Valley's typical home value of $2.18 million stands in stark contrast to surrounding flat-land neighborhoods.

- Cambrian Park: Typical values range from $1.82M to $2.45M.

- Willow Glen: Typical values average $1.84M.

- White Oak: Typical values average $1.52M.

- Blossom Valley: Typical values average $1.42M.

- Santa Teresa: Typical values average $1.35M.

- Edenvale - Seven Trees: Typical values average $1.11M.

Part 2: The $2.5 Million Pricing Ceiling

While single-family detached homes in Almaden remain in high demand, the sub-market has become incredibly sensitive to price thresholds . Real-time transaction data reveals a clear "split" in market speed based on a home’s price point:

- Under $2.5 Million (The High-Velocity Zone): Turnkey homes priced below $2.5M are highly competitive, routinely attracting multiple offers and going pending in 11 to 14 days. Mid-tier homes priced under $2.0 million regularly spark bidding wars and sell well above asking price.

- Over $2.5 Million (The Slower-Velocity Zone): High-end luxury estates listed over $2.5M are spending much longer on the market, often stretching past 40 days. Buyers in this upper tier have successfully negotiated price drops before closing.

Real Realized Value: Recent Foothill Home Sales (June to July 2026)

- 6149 Royal Acorn: Listed at $1.99M, sold for $2.25 million (+12.5% over list) in 0 days.

- 6394 Menlo Dr: Listed at $1.59M, sold for $1.63 million (+1.9% over list) in 71 days.

- 1112 Grimley Ln: Listed at $2.84M, sold for $3.00 million (+5.2% over list) in 40 days.

- 6399 Farm Hill Way: Listed at $2.85M, sold for $2.80 million (-1.7% below list) in 41 days.

- 20041 Mann Oak Ct: Listed at $3.99M, sold for $3.95 million (-1.2% below list) in 43 days.

- 7150 Calcaterra: Listed at $2.58M, sold for $2.40 million (-7.2% below list) in 33 days.

- 5951 Post Oak Cir: Listed at $1.498M, sold for $1.35 million (-9.8% below list) in 36 days.

Part 3: The K-Shaped Tech Wealth Shift

Almaden Valley’s high-end real estate has historically been fueled by Silicon Valley tech compensation . In 2026, tech wealth is reorganizing, creating a "K-shaped" purchasing power spectrum among buyers:

- The AI Capex Boom (The High End): Tech giants like Amazon, Microsoft, Alphabet, and Meta are dedicating over $700 billion to AI infrastructure in 2026 . Professionals and executives capitalizing on this targeted AI growth hold massive liquid wealth, allowing them to make highly competitive, cash-like offers on luxury foothill estates.

- Legacy Tech Consolidation (The Mid-Tier): To fund their AI transition, tech companies have cut over 142,000 to 150,000 corporate and administrative jobs in the first half of 2026 . This includes major layoffs at Oracle (21,000 positions), Amazon (16,000 corporate roles), Meta (8,000 roles), Microsoft (4,800 roles), and Cisco (under 4,000 roles).

- The Mortgage "Lock-In" Penalty: On top of job shifts, many current homeowners in Almaden are holding onto interest rates near 3.0% . Trading their current house for a new home at today’s rates (around 6.2% to 6.8%) can add $3,000 a month in extra payments. This financial penalty has kept single-family home listings exceptionally thin, forcing buyers to compete fiercely for any new inventory.

Part 4: Geohazards & The NHD "Paperwork Shield"

The gorgeous natural landscape that makes Almaden Valley so desirable also exposes it to geographical risks. Navigating these factors transparently is your greatest legal shield when transacting real estate:

- Wildfire & Flood Exposure: Approximately 99% of Almaden Valley properties lie in state-designated moderate to high wildfire hazard zones. Furthermore, 33% of the neighborhood’s parcels are situated in severe flood zones along local mountain runoffs like Alamitos Creek.

- Civil Code Section 1103 (The NHD Report): Sellers are legally required to provide buyers with an independent, third-party Natural Hazard Disclosure (NHD) Report. This mandatory statutory document maps out exactly whether the property sits in a fire, flood, landslide, or earthquake zone.

- The "As-Is" Misconception: You cannot use an "as-is" contract clause to waive the buyer's right to receive this hazard report. Delivering this paperwork early prevents buyers from backing out during active escrow or filing post-sale lawsuits.

Part 5: Mastering a Tough Home Insurance Market

Because major home insurance carriers like State Farm, Allstate, and Farmers have capped or non-renewed thousands of policies in California's fire-prone areas, securing coverage requires a clinical, strategic approach:

- FAIR Plan Price Hikes: Homeowners who cannot find traditional coverage rely on the California FAIR Plan. However, effective October 15, 2026, the California Department of Insurance has approved a 29.1% average statewide rate increase.

- The Foothill Premium Surcharge: Because this is a statewide average, homes with high wildfire exposure in the foothills are at the extreme end of the hike, the wildfire-peril portion of their premiums is expected to double.

- Companion DIC Policies: The FAIR Plan is a "named-peril" safety net that only covers basic fire damage. To protect your home, you must purchase a companion Difference in Conditions (DIC) policy to cover water damage, theft, and personal liability.

- Smart Premium Discounts: Homeowners can secure up to 12 different home-hardening and community discounts (such as installing ember-resistant vents or establishing a 5-foot non-combustible buffer zone around the home) to save up to 16.4% off the wildfire portion of their bill.

- Private Market Movement: Some private insurers are quietly re-entering specific ZIP codes under California’s new Sustainable Insurance Strategy. Working with a local independent broker can help you find tailored private policies that offer broader coverage at a lower cost than the FAIR Plan.